4.0 SOCIO - ECONOMIC FEATURES

4.1 POPULATION CHARACTERISTICS

4 1.1 Maine and the New ngland Region

4 1.2 Merrymeeting Bay and the Surrounding Region

4 1.3 The Surrounding Counties

4.1.4 The Surrounding Towns

4.1.5 Population Projections

4 1.6 Planning Implications

4.2 INCOME CHARACTERISTICS

4.3 EMPLOYMENT AND LABOR FORCE

4.4 ECONOMIC ACTIVITY

4.4.1 Overview

4.4.2 Resource-Based Industries

4:4:3 Manufacturing

4.4.4 Contract Construction Industries

4.4.5 Service Industries

4.4.6 Brunswick Naval Air Station

4 4.7 Wholesale and Retail Sales

4.4.8 Summary of Planning Implications

4.5 TAXATION

4.5.1 The Rise of Property Taxes: 1960-1973

4.5.2 Impacts of Property Taxation on the Elderly and Low Income

Landowners

4.5.3 Property Tax Pressures and the Loss of Farms

4.5.4 Tax Pressures as Incentives to Attract Business

4.5.5 Tax Pressures and Forest Lands

4.5.6 Summary of Planning Implications

4.6 REFERENCES

Population growth trends in New England and Maine have taken a

significant change of direction since the last census in 1970 (see

Table Between 1960 and 1970, New England's population had grown from

10,510,106 to 11,847,186, a 12.7% increase. The nation as a whole

increased by 13.3%. Maine, the slowest growing state in New England,

increased by merely 2.5%. Almost as many people left the state as

were born in it. The natural increase (births minus deaths) numbered

approximately 94,000 between 1960 and 1970; while the net migration

tin-migration minus out-migration) totaled nearly-70,000. That is,

migration resulted in a net loss of population to the state (Dearborn

and Daigle 1972).

Recent figures (Ploch 1974) show that within New England a population

shift may be occurring from Connecticut, Rhode Island, and

Massachusetts to Maine, New Hampshire, and Vermont. Growth rates in

southern New England for the period 1970 to 1974 range from 1.7 to

2.2 percent; whereas in the northern states, growth is increasing at

rates from 5.5 percent in Maine and 9.5 percent in New Hampshire.

In-migration from other states outside of the New England area to

northern New England is also likely, especially in light of the fact

that these states (Maine, New Hampshire, and Vermont) were the only

ones north of the Mason-Dixon line and east of the Rockies to exceed

the U.S. average growth rate for that period (Ploch 1974).

The Merrymeeting Bay area, as defined by this study, encompasses

eight towns (Bath, Bowdoin, Bowdoinham, Brunswick, Dresden, Richmond,

Topsham, and Woolwich) and parts of three counties (Sagadahoc,

Lincoln, and Cumberland). This section will detail population trends

within the three counties and the surrounding towns respectively.

1960 1970 Change 1974 * % Change * Population Population 1960-70 Population 1970-74 MAINE 969,265 993,663 2.5 1,047,000 5.5 Cumberland Co. 182,751 192,528 5.4 . 199,800 3.7 Lincoln Co. 18,497 20,537 11.0 22,200 8.2 Sagadahoc Co. 22,793 23,452 2.9 26,500 9.4 NEW ENGLAND 10,510,106 11,847,186 12.7 12,536,128 2.7 UNITED STATES 179,323,175 203,184,772 13.3 -- -- * Estimated SOURCES: Dearborn and Daigle 1972; Dearborn 1974; Ploch 1974.

Growth As with the state as a whole, population trends in Sagadahoc

and Cumberland counties have recently taken an upward turn. Between

1960 and 1970, these two counties experienced a net out-migration,

despite their high growth rate relative to the rest of the state.

From 1970 to 1974, this trend reversed itself and a net in-migration

resulted (see Table 4-1 and 4-2). The result was higher growth rates

and the most striking change occurred in Sagadahoc County, where the

growth rate jumped from 2.9% during 1960 to 9.4% in just the first

four years of the 1970s. Similarly, Cumberland County is well ahead

of its previous growth rate (5.4 from 1960-1970) with a 3.7% increase

since 1970 (Dearborn 1974),

Lincoln County has been one of Maine's fastest growing counties since

1960. Between 1960 and 1970, it experienced a net in-migration of

1,323 persons, and grew a total of 11 percent (while Maine as a whole

grew only 2.5 percent). Between 1970 and 1974, it continued to grow

at an even faster rate, 8.2 percent in just four years (Dearborn

1974). Relative to other counties in Maine, Lincoln and Sagadahoc

counties still currently rank among the fastest growing. In 1970

Sagadahoc County ranked ninth in the state in terms of growth rates;

Lincoln County, third; and Cumberland County, seventh. By 1974

Sagadahoc County rose to fourth fastest growing while Lincoln dropped

to sixth and Cumberland twelfth .

Population Distribution

In 1970 the population in both Cumberland and Sagadahoc counties was

predominantly urban (62.7 and 62,8 percent respectively) while

Lincoln County in contrast was 100 percent rural. A comparison with

1960 figures shows that Cumberland County lost in urban percentage in

the ten year period while Sagadahoc County gained, and Lincoln

remained the same (Dearborn and Daigle 1972). Figures showing the

population distribution since 1970 are not available. However, some

perceive a reversal of the national trend towards urban concentration

evidenced in the 1960s. Rural areas in Maine seem to be attracting

more households in the early 1970s than urban areas.

Components of Population Change Since 1970 1970-1973* 1970 Natural Net 1973* Population Increase : Migration : Population MAINE 93,663 25,842 19,495 1,039,000 Cumberland Co. 92,528 3,800 900 97,200 Lincoln Co. 20,537 100 1,000 21,600 Sagadahoc Co. 23,452 700 800 24,900 * Estimated SOURCE: Dearborn 1974.

Peak Seasonal Population

The state of Maine is known to experience a substantial

populationincrease in the summer season. In 1970 it has: been

estimated thatthe peak seasonal increase added one-half million

people to the state,a 50% increase over the permanent year round

population (Veazie 1972).

Within the Merrymeeting Bay area, in 1970, Cumberland County

increased by an estimated 45%, Lincoln County by 133%, and Sagadahoc

County by 31% (Veazie 1972). See Table 4-3. Relatively little of this

increase concentrated in the towns immediately surrounding the Bay.

The majority of it occurs on the coast and in the coastal towns.

Their total population increased an estimated 15% (see also

discussion below under The Surrounding Towns).

Population Growth

Between 1960 and 1970, the population of the towns surrounding

Merry-meeting Bay grew collectively by 3%. Two towns, Bath and

Richmond, experienced a decline in population (by-10% and-17%

respectively), while all other towns exceeded the state average

growth rate in that decade. Four towns, Topsham, Bowdoin, Woolwich,

and Bowdoinham, grew faster than the national growth rate of 13.3%.

These towns increased by 32%, 28&, 21% and 15% respectively (see

Table 4-4 ).

Since 1970, there is evidence from the increased number of housing

starts (see Chapter 6.0, Section 6.4) that the towns around the Bay

are experiencing a significant increase in population. The town of

Richmond, for example, issued two building permits in 1970; in 1973

the number jumped to 26. Another indication of increased population

pressures in the area is the trend in real estate values which have

risen sharply since 1970 (see Chapter 6,0, Section 6.4).

Peak Seasonal Population

In 1970, the towns around Merrymeeting Bay experienced an estimated

15% increase in population during the peak season (summer). The town

with the largest individual percentage increase was Brunswick (24%)

followed by Richmond (17%), Bowdoinham (13%), Woolwich (12%), Dresden

(s%), Bath (7%), Bowdoin (4%), and Topsham (3%) (Veazie 1972). These

increases are small in comparison to those experienced by the

surrounding counties (see Table 4-3).

TABLE 4-3

PEAK SEASONAL POPULATION ESTIMATES 1970 Year Round Seasonal Peak Seasonal Population Increment : Increase : Population MAINE 993,663 506,725 51 1,500,388 Cumberland Co. 192,528 87,093 45 279,621 Lincoln Co. 20,537 27,293 133 47,830 Sagadahoc Co. 23,452 7,380 31 30,832 MERRYMEETING BAY 37,710 5,522 15 43,235 Bath 9,679 650 7 10,329 Bowdoin 858 38 4 896 Bowdoinham 1,294 166 13 1,460 Brunswick 16,195 3,866 24 20,061 Dresden 787 74 9 861 Richmond 2,168 362 17 2,530 Topsham 5,022 158 3 5,180 Woolwich 1,710 208 12 1,918 1. Seasonal Increment: year round. SOURCE: Veazie 1972.

Migration Characteristics

Tables 4-5 and 4-6 show the residence changes in the Bay area for the

periods 1955-1960 and 1965-1970. Between 1955 and 1960, some 19.6

percent of the 1960 resident population had moved into the area from

out of state, or about 6,400 persons. Twenty-nine percent had moved

into the area from elsewhere in Maine, and the remaining 51.4 percent

were residents of the area prior to 1955. Brunswick showed the

greatest out of state influx for that period, some 33.8 percent or

nearly 4,750 persons. This can probably be attributed to the

Brunswick Naval Air Station and Bowdoin College. Elsewhere in the

area, Woolwich, Bath, and Dresden showed influxes of 8.8 percent, 7.7

percent, and 7.3 percent respectively.

By 1970, the percentage of the residents which had moved into the

area from out of state during the prior S-year period had risen to

20.9 percent. This represents some 7,200 persons as compared to the

1955-1960 influx of 6,400 persons. While the overall change is not

significant, the distribution of the influx is. Bath, Bowdoinham,

Bowdoin, and Topsham showed significant influxes as compared to the

1955-1960 period. Dresden and Richmond also saw an increase, but not

as significant, while Woolwich and Brunswick showed a decreasing

out-of-state influx. Map 9 depicts these

changes.

With the recent increases in total population (1970-1974, see Table

4-1), it is expected that the towns surrounding the Bay, especially

Richmond, Bowdoinham, Bowdoin, and Topsham, will continue to grow at

a faster rate and will continue to absorb more out-of-state influx

than it has in the past.

RESIDENCE CHANGES 1955-1960 (1) (persons 5 years and older) Present Same DIFFERENT HOUSE IN MAINE OUT OF STATE Residence Total House Same Co. Diff. Co. % Total Diff. State Abroad % Total Bath 9,636 5,349 2,548 606 32.7 624 124 7.7 Bowdoinham 997 682 173 95 26.8 43 -- 4.3 Bowdoin 537 372 60 90 27.9 10 -- 1.8 Brunswick 14,098 5,373 2,368 1,192 25.3 4,319 457 33.8 Dresden 782 481 90 154 31.3 57 -- 7.3 Richmond 1,880 1,090 397 285 36.3 77 27 5.5 Topsham 3,302 1,659 460 618 32.6 482 53 1.6 Woolwich 1,271 837 250 34 22.3 112 -- 8.8 TOTAL 32,503 15,843 6,346 3,074 29.0 5,724 661 19.6 (1) Shows place of residence 5 years prior to the 1960 census. SOURCE: U. S. Population Census.

RESIDENCE CHANGES 1965-19701 (persons 5 years and older) Present Same DIFFERENT HOUSE IN MAINE OUT OF STATE Residence Total House Same Co. Diff. Co. % Total Diff. State Abroad % Total Bath 8,866 4,948 1,762 750 28.3 l,013 175 13.3 Bowdoinham 1,214 789 169 94 21.6 162 -- 13.3 Bowdoin 729 486 88 21 14.9 115 12 17.4 Brunswick 14,728 5,664 2,459 1,301 25.5 4,120 386 30.6 Dresden 822 542 95 82 21.5 98 -- 11.9 Richmond 2,037 1,028 380 380 37.3 168 7 8.5 Topsham 4,531 2,298 727 528 27.7 807 49 18.9 Woolwich 1,453 967 336 36 25.6 73 -- 5.0 TOTAL 34,380 16,722 6,016 3,192 26.8 6,556 629 20.9 1. Shows place of residence 5 years prior to the 1970 census. SOURCE: U. S. Population Census.

Generally, population projections made prior to 1970 for the

decade between 1970 and 1980 have fallen short of the trends

evidenced by the recent figures for 1974 (Dearborn 1974). The Maine

State Planning Office projected that between 1970 and 1980 Sagadahoc

County would grow by 24.2%, Lincoln County by 10.7%, and Cumberland

County by 7.2% (State Planning Office 1973). We have seen previously

that Sagadahoc County has grown by 9.4 in the first four years of the

decade alone, that Lincoln County had grown by 8.2% by the end of

1974, and that Cumberland County had grown by 3.7% in this

period.

Obviously there are forces at work which have resulted in an

unexpected acceleration of population growth in Maine and the

Merrymeeting Bay area since 1970. With the completion of I-95 along

the western edge of the Bay, we believe this growth trend will be

even more dramatically increased in the towns surrounding the

Bay.

The preceding examination of population characteristics and trends

in the Merrymeeting Bay area points to the following:

1. The population of the area is growing at an unexpected and

accelerating pace due to a large influx of out of staters. It is

suspected that many seek a rural atmosphere such as that found in the

towns surrounding the Bay. Advanced planning will be needed if the

Bay towns are to retain their rural undeveloped character while

absorbing the new growth. Chapter 6 details the planning implications

of growth in terms of development trends.

2. Seasonal population increases in the Bay towns are insignificant

compared to seasonal increases which occur in the adjacent coastal

towns. The Bay is not seen as an attraction to tourists at

present.

missing text #100 - 105

PLACES OF WORK OF MERRYMEETING BAY RESIDENTS 1970 Total Andros. Cumberland Co. Sagadahoc Co. Lincoln KennebecKnox Other & Residence Workers County Ptld. Other(l)Bowdoin Topsham Other(2)County County Co. Not Rep. Bath 3,542 21 30 462 21 2,703 109 22 174 Bowdoin 291 57 84 89 33 28 Bawdoinham 467 16 115 7 254 46 29 Brunswick 6,618 102 186 4,311 na na 839 67 46 1,067 Dresden 339 na na 121 112 88 18 Richmond 804 47 7 5 446 22 172 105 Topsham 2,043 54 49 890 456 354 34 9 197 Woolwich 570 6 93 12 403 20 9 27 TOTAL 14,674 281 294 5,960 89 529 5,148 364 383 9 1,617 1. Primarily Brunswick 2. Primarily Bath SOURCE: U. S. Census of Population.

The period from 1960 to 1973 saw a dramatic shift in the growth

rate of major economic sectors in Maine. Manufacturing, for example,

while remaining the dominant sector in terms of number of jobs

generated in 1973 (employing some 109,650 out of 398,600 persons),

nevertheless recorded a negative growth rate (-3.5%). The fastest

growing sectors emerged as service industries (+78.7%); government

(+65.3%); finance, insurance, and real estate (+48.8%); and trade

(+37.3%). Transportation and public utilities sectors declined by

2.1%, manufacturing by 3.5%, and agriculture by an undetermined

amount (see Table 4-12).

In the Merrymeeting Bay region (Sagadahoc, Lincoln, and Cumberland

counties), a predominance of jobs were held in the wholesale/retail

trade sector, service sector, and manufacturing sector in 1970, with

a trend towards the increase of the public administration,

govern-mental sector, construction sector, service and trade sectors.

While manufacturing declined in general in this tri-county region, it

showed an increase in Sagadahoc County (see Table 4-13).

In the towns immediately surrounding Merrymeeting Bay, of a total of

13,558 jobs in 1970, 4,P42 were held in the manufacturing sector,

3,373 in the service sector, 2,136 in wholesale and retail trade

sector, 847 in public administration and government, 882 in

construction industries, 525 in the transportation, utilities sector,

and 299 in primary resource industries (forestry, agriculture,

fishing, and mining; see Table 4-13). The 1960-1970 trends showed the

greatest relative increase in construction industries (+66.4%

followed by public administration and government, 48.3%),

utilities/transportation (+34.5%), service industries (+32.6%), and

trade (+20.4%). Manufacturing had slowed to a 2.1 % increase over

1960, and resource industries had declined 13,5% from 1960 (in number

of jobs , see Table 4-13 and 4-14). The more significant economic

sectors, both past (resource-based industries and manufacturing) and

present (wholesale and retail trade, services, construction, and

government) will be discussed in detail in the following

paragraphs.

JOBS BY INDUSTRY Maine Trends 1960--1973 % Change Change % Change 1960 1970 1971 1973 1960-1970 1960-1973 1970-1973 Agriculture 21,900 14,400 13,000 n.a. -34.2 n.a. n.a. Manufacturingl 113,670 117,750 108,920 109,650 + 3.5 -3.5 -6.8 Leather 24,100 25,810 22I690 20,150 + 7.0 -16.4 -21.9 Paper, Allied Prod. 18,150 17,730 16,830 17,780 -2.3 -20.4 0.2 Lumber, ood Prod. 16,900 14,200 13,480 13,640 -16.9 -19.3 -3.9 Food, Food Prod. 11,400 11,490 11,650 10,630 + 0,7 -6.8 -7.4 Textiles 14,100 10,900 8,860 9,360 -22.6 -33.6 -14.1 Shiplbuilding, Transp. 14,360 12,330 10,660 10,100 -29.7 -18.0 Trade 53,900 65,920 67,690 74,010 +22.3 +37.3 +12.2 Wholesale 14,550 14,330 14,400 15,520 +6.7 +8.3 Retail 39,350 51,590 53,290 58,490 +31.1 +48.6 +13.3 Government 39,030 59,040 62,540 64,520 +51.2 +65.3 +9.2 Finance, Insur., and Real estate 9,000 12,210 12,660 13,390 +35.6 +48.8 +9.6 Real Estate 1,410 1,780 1,760 1,670 -26.2 +18.4 -6.1 Transportation, Publ. Utilities 18,100 17,540 17,460 17,720 -3.0 -2.1 -1.0 Contract Construction 13,600 16,820 17,000 19,440 +23.6 +42.9 +15.5 Service 30,200 42,930 45,990 53,960 +42.1 +78.7 +25.6 SOURCE: Maine Department of Commerce and Industry 1974.

JOBS BY INDUSTRY 1970 Merrymeeting Bay Region Fin. ResourceContract Util/ Insur. Publ.Adm/ Indus. Const. Mfg. Trans. Trade R.Est. Service Govt. TOTAL(1) MAINE -- 16,820 117,750 17,540 65,920 12,210 421930 59,040 -- Sagadahoc Co. 364 305 31946 220 864 119 1,976 1,568 9,362 Lincoln Co. 727 1,281 713 198 1,203 145 1,656 957 6,88Q Cumberland Co. 1,400+ 4,868 191408 6,057 22,952 6,319 22,384 11,679 95,067 MERRYMEETING BAY299 882 4,442 525 2,136 -- 3,373 847 13,558 Bath 43 183 1,333 220 576 -- 772 244 3,644 Bowdoin 30 42 99 5 15 -- 67 17 279 Bowdoinham 19 24 163 16 64 -- 100 35 453 Brunswick 80 349 1,394 154 1,013 -- 1,699 349 5,541 Dresden 45 33 105 21 37 -- 60 21 35? Richmond 26 62 381 40 48 -- 175 67 851 Topsham 40 154 717 28 286 -- 371 82 1,824 Woolwich 16 35 250 41 97 -- 129 32 609 1. TOTAL for the towns includes other miscellaneous industries in addition to those listed. SOURCES: U. S. Census of Population Curtis Harris, University of Maryland in TRIGOM 1974. Maine Department of Commerce and Industry 1974.

In the Merrymeeting Bay region, broadly including Sagadahoc, Lincoln,

and Cumberland counties and more narrowly defined as the towns

adjacent to the Bay, resource-based industries include agriculture,

mineral extraction, and forestry. (This category of industries does

not include the manufacture of products from resources such as paper

from wood). The importance of these industries in generating job

opportunities and in contributing valuable products to the rest of

the state (or nation) is discussed below.

In general, resource-based industries have historically been

declining in activity relative to other industries in Maine. Since

1940, the number of jobs in the state in agriculture, forestry, and

fisheries has declined from 40,700 to less than 15,000 in 1970

(American Forestry Institute 1972). In the last decade alone, Maine

as a whole experi-enced a 34.2% drop in the number of jobs in the

agricultural sector, and a 16.9% drop in jobs in the lumber and wood

products (excluding paper) industries (see Table 4-14).

In the Merrymeeting Bay region, since 1960, Sagadahoc County as a

whole has experienced no change in the number of resource-based jobs;

Lincoln County has experienced an increase of 8.9%; and Cumberland

County a decrease of 19%. Within the Bay Study Area, the towns of

Bowdoinham, Brunswick, Richmond, and Woolwich have experienced a net

loss in the number of resource-based jobs while Bath, Bowdoin,

Dresden, and Topsham have had an increase. Overall, these towns have

lost 13.5 percent of the total resource-based jobs since 1960 (see

Table 4-14). There is little information on resource-based industry

avail-able at the town level. However, the report of the Dresden

Planning Board (1971) described the decline of these in that town and

is probably indicative of the trends being experienced by all small

towns around Merrymeeting Bay:

For a great many years the townspeople of Dresden were their own

bosses. They farmed the land, raised most of what they needed for

food, clothing and other necessities of life and they were happy...As

the surrounding areas, have over the past two

JOBS BY INDUSTRY Percent Change 1960-1970 Fin. ResourceContract Util/ Insur. Publ.Adm./ Indus. Constr. Mfg. Trans. Trade R.Est. Service Govt. TOTAL MAINE + 23.6 + 3.5 - 3.0 + 22.3 +35.6 + 42.1 + 51.2 Sagadahoc Co 0.0 - 4.5 +18.8 -16.0 -17.4 +30.5 +335.5 +16.3 Lincoln Co. + 8.9 +137.2 -54.8 -37.3 + 22.0 + 42.6 +208.7 +10.4 Cumberland Co. -19,0 + 22.4 +29.3 + 2.2 + 53.1 +86.6 + 59.1 + 61.0 +44.7 MERRYMEETING BAY -13.5 + 66.4 + 2.1 + 34.6 + 20.4 + 32.6 + 48.3 +15.9 Bath +65.3 + 45.2 -22.5 + 61.7 + 0.6 + 6.6 + 79.4 -7.4 Bowdoin +87.5 +250.0 +17.8 + 36.3 +219.0 + 41.6 +78.8 Bowdoinham -64.1 +200.0 +13.9 +100,0 +220.0 + 25.0 +191.6 +35.1 Brunswick -29.2 + 63.8 +12.6 6.6 + 26.4 + 41.3 + 40.7 +24,8 Dresden +2S.5 + 94.1 + 23.3 + 56.5 -38.2 +18.2 Richmond -36.5 + 40.9 +12.0 + 60.0 -29.4 + 9.2 + 26.4 + 8.2 Topsham +25.0 + 87.8 +32.7 -30.0 + 47.4 + 42.6 + 36.6 +45.6 Woolwich -46,6 + 25.0 +52.4 +156.2 + 25.9 +180.4 + 60.0 +28.7 SOURCES: Table 4-13 U. S. Census of Population 1960

centuries, grown requiring the various services of laborer, clerical

worker or professional, the makeup of the Town of Dresden has changed

from one of farmers and fishermen to nearly a completely residential

area-the bedroom for such areas and activities as the Bath Iron

Works, Brunswick Naval Air Station, Central Maine Power, U. S.

Veterans Administration at Togus, the State of Maine, factories and

mills in Augusta, Gardiner, Richmond, and Wiscasset.

The following paragraphs will discuss in detail the various types of

resource-based industries and their role in the economy of the area,

past, present, and future.

Agriculture

The land surrounding Merrymeeting Bay is low and gently rolling, and

gradually becomes hummocky as higher elevations are reached upland.

Near the Bay, floodplain soils and glacial till deposits form some of

the most productive agricultural soils in the state. Because of the

low flat character of this area, areas of Class I and Class II

agricultural soils from 50 to 100 acres in size can be found along

the Bay on Green Point, Abagadasset point, and Pleasant Point. As one

proceeds upland the hilly character of the land reduces the size of

the Class I and II areas, making such areas less prime for large

farming operations.

Overall, farm activity in the Merrymeeting Bay region (Sagadahoc,

Lincoln, and Cumberland countries) has been steadily declining. The

number of farms in Sagadahoc County (which includes most of the Bay

towns) dropped from 253 to 113 during the five-year period from 1964

to 1969; and it is estimated that the number has since fallen to 94

(see Tables 4-15 and 4-16). The total acres in farmland dropped from

37,000 to 1B,542 between 1964 and 1969 while the average size per

farm increased slightly from 146.6 to 155.2 acres. During this time,

farm values (per acre) in Sagadahoc County rose 29 percent. Similar

trends are evidenced in Lincoln and Cumberland counties; except that

in Cumberland County, the average size of farms declined. This

probably resulted from the fact that the number of 1000+ acre farms

dropped from 9 to 6, while in Sagadahoc and Lincoln counties, the

number of farms in this size class either increased or remained the

same.

FARM INDICATORS-MERRYMEETING BAY 1974 Estimates Sagadahoc Co. Lincoln Co. Cumberland Co. 1969 1974 1969 1974 1969 1974 Number of farms 113 94 195 163 536 448 Average size (ac.) 155.2 1 .58.3 166.3 169.6 125.8 128.3 Average Value of Land/Buildings per acre 190 324 222 379 282 482 SOURCE: Maine Department of Agriculture, unpublished estimates 1975.

Estimates on farm size and value for the period since 1969 are also

found in Table 4-16. These estimates were derived by taking 1974

state figures and applying the trends evidenced by these to the

individual counties. Since the number of farms statewide has dropped

16.5% between 1969 and 1974, the number of farms in each of the

counties in the Merrymeeting Bay area is assumed to have declined by

this percentage also (Maine Department of Agriculture, unpublished

data 1975).

There is little information on farm activity available at the town

level. However, the Dresden Planning Board report of 1971 indicates a

serious decline which is probably typical of all towns around the

Bay. By the Spring of 1969, only one dairy farm remained within the

town, although a few herds of beef, replacement or breeding stock

were to be seen...The town, once principally characterized by open

fields and pasture land, has returned to its eighteenth century

woodlands.

The decline in agricultural activity can probably be attributed to a

number of factors including rising real estate values, declining farm

products prices, increasing costs of farm supplies (such as feed,

fertilizer, machinery, baling twine, etc.),poor market development

and an increase in the number of work options available. Perhaps one

of the most serious problems is the growing disparity between farm

income and expenditures. In Sagadahoc County in 1969, eighteen out of

twenty-two farms with sales greater than $40,000 had expenses greater

than $40,000 and in general, most farms had expenditures equal to or

greater than half the total sales (see Table 4-1'7).

The farms most seriously affected are those represented by sales less

than $20,000. Between 1964 and 1969, forty out: of sixty-four farms

in this sales class dropped out of production (or to below sales of

$2,500 per year) in Sagadahoc County; fifty-nine out of 110 were

eliminated in Lincoln County, and 100 out of 245 were lost in

Cumberland County (see Table 4-18).Those with sales of $20,000 or

more remained stable. In the recent past, livestock growers and dairy

farmers have been particularly hard hit by rising feed costs. This

problem stems in part from national sales of grains to foreign

countries coupled with the increased costs of transportation from the

Midwest which have reduced supplies and increased costs.

The high cost of product to consumers caused by high mark-up by

distributors has contributed to another trend in the area: the

increase of small scale organic gardening. As local-based cooperative

food markets continue to develop, these small scale producers will

find better markets and may help slow the trend of declining farm

activity.

FARM SALES AND EXPENDITURES 1969 Sagadahoc Co. Lincoln Co. Cumberland Co. SALES $ 40,000+ 22 23 81 20,000-39,999 13 26 67 10,000-19,999 7 18 50 5,000-9,999 3 15 42 2,500' 4,999 14 18 53 EXPENDITURES $ 40,000+ 18 24 71 20,000-39,999 16 17 47 10,000-19,999 6 18 63 5,000-3,999 12 21 52 2,000-4,999 5 13 40 SOURCE: U. S. Census of Agriculture 1969 (Maine Department of Agriculture)

FARM INCOME AND SALES Merrymeeting Bay Region 1964-1969 Sagadahoc Co Lincoln Co Cumberland Co 1964 1969 1964 1969 1964 1969 No. farms by sales of $40,000+ 26 22 26 23 77 81 $20,000'39,999 10 13 36 26 87 67 $10,000-19,999 22 7 32 18 95 50 $ 5,000' 9,999 22 3 36 15 73 42 $ 2,500' 4,999 20 14 42 18 77 53 Market Value-all prod. 2,760,650 2,417,661 4,059,750 5,111,295 ll,163,500 11,827,223 Av.per farm ($) 10,912 21,395 9,759 26,211 12,700 22,065 Crops ($) 276,699 238,547 314,769 254,063 2,377,677 2,080,669 Forest Products ($) 35,930 6,121 93,384 31,450 170,815 53,596 Livestock, Poultry & Products ($) 2,446,465 2,172,993 3,628,016 4,825,782 8,585,383 9,692,958 SOURCE: 1969 Census of Agriculture--County Data, Maine Depautment of Agriculture

Other problems affecting the farming sector in addition to increasing

costs of production, declining farm product prices, and poor markets

include increasing land values and difficulty in obtaining financing.

The state Farm and Open Space Land Law reduces the tax pressure on

farmlands which might result as land values increase due to

development pressures (see Section 4.5). However, the declining

profitability of farming, the difficulty of obtaining financing to

overcome short term losses, and the increasing profitability of real

estate sales are combining to increase the number of farmers who are

opting to drop out of production and sell part or all of their land

for residential or commercial uses. The result is a loss in the

agricultural resource capabilities of the area, and of the state as a

whole. This loss will be, unfortunately, irreversible if farmland is

committed to residential or commercial development. In the past,

farmers who found agricultural production uneconomical often

abandoned their fields which then eventually reverted back to

woodland. The town of Dresden is a case in point. However, as the

demand for developable land may increase with the completion of I-95,

the option of capitalizing on now desirable open lands could result

in the permanent loss of valuable agricultural land. It should be

noted that while most farmers feel that agricultural productivity

should be maintained and enhanced, many also feel that landowners

should be allowed to do what they wish with their own land.

Finding a solution which will at once conserve the prime agricultural

resources of the area yet avoid penalizing the farming sector, which

now feels more than most sectors the impacts of a depressed economy,

will involve combining regulatory mechanisms such as zoning and

financial incentives such as the formation of Community Development

Corporations-(CDC). A CDC could assist farmers in forming marketing

cooperatives, providing community grain storage areas, providing

credit and financing, the formation of farm cooperatives which could

pool labor and equipment, providing educational services, and

lobbying for farm interests at the state level. Another approach

might be the encouragement of additional state action in easing the

financial roadblocks many farmers now face. Presently there is some

relief available through FHA and a State Production Credit program,

but more is needed. The State Development Office could well be the

vehicle to establish a farm credit program which could assist farmers

in providing low interest loans to offset the temporary setbacks

caused by inflation or recession or to establish cooperatives as

mentioned above.

Still another approach is suggested in a report recently issued by

the Connecticut Governor's Task Force for the Preservation of

Agricultural Land. This report recommended the state preserve enough

farm-land to produce one-third of the foodstuff its people require

(this amounts to 325,000 acres in Connecticut). It further recommends

that the state should buy development rights to those acres' while

leaving the farms in their present ownership; and that the purchase

will require a bond issue of $500 million to be retrieved by a 1% tax

on real estate transfers.

Forestry

Almost 90 percent of the state of Maine is covered by commercially

valuable forests (see Table). In the past ten years, the amount of

forested land has increased by 3% from 17.2 million acres to 17.7

million acres. Despite this trend, in Sagadahoc, Lincoln, and

Cumberland counties, which surround Merrymeeting Bay, commercial

forest lands have declined since 1959 from 889,000 acres to 778,300

acres (see Table 4-19).

Ownership of commercial forests in the state as a whole is dominated

by large forest industries. These industries own approximately 49% of

Maine's commercial forests while public agencies own less than 2%;

farmers 6.5%, and other private owners 43%. In the Merrymeeting Bay

region, the ownership pattern is quite different with a majority

being owned by private interests (88%); 10.6% by farmers; 1.2% by

public agencies; and none by forest industries (see Table 4-20).

Logging activity for most of the Merrymeeting Bay study zone has been

significant. In the last ten years, all but a very few areas have

been commercially cut. In 1971, Sagadahoc, Lincoln, and Cumberland

counties produced 21,422 thousand board feet of saw logs and 97,700

rough cords of pulpwood. It is not known how much of this came from

within the study area. Sagadahoc County, which includes a majority of

the study area, is notably the lowest producer of the three counties,

however (see Table 4-21). Since 1960, it has averaged an annual

production of over 2.5 million board feet of saw logs and 18,000

rough cords of pulpwood (Veazie 1973).

As most of the commercial logging within the area is done by small

commercial operators, paid by a private landowner, cutting operations

occur in an in-and-out manner; often without regard to proper forest

management. Erosion and damage to the future productivity of the

forest system under such conditions are frequently the result. Table

4-22 describing the acres of various stand size classes indicates

that a majority of the area in Lincoln, Sagadahoc, and Cumberland

counties is covered with saplings and seedlings. This class of stand,

which generally reflects overcutting, a lack of planning for future

productivity, abandonment of agricultural fields, and poor markets

will require an accelerated program of forest management to improve

the quality and growth rate (SCS 1974).

Presently there are two service foresters and one district forester

(Bureau of Forestry) employed in the Merrymeeting Bay area whose

primary function is to assist small woodlot owners (500 acres or

less, see also Chapter 7, section 7.3).

AREA OF COMMERCIAL FOREST LAND 1959-1971 (thousand acres) 1959 1971 Area %Total Area %Total Sagadahoc County 141 86 130.3 79 Lincoln County 245 84 217.4 76 Cumberland County 503 89 430.6 77 MAINE 17,169 86 17,748.6 89 SOURCES: Ferguson and Longwood 1960 Ferguson and Kingsley 1972.

OWNERSHIP OF COMMERCIAL FORESTS RESOURCES 1971 (000 acres) Public Private Total Farmer Other Sagadahoc County 2.3 14.8 113.2 130.3 Lincoln County 17.5 199.9 217.4 Cumberland County 6.4 50,2 374.0 430.6 TOTALS 8.7 82,5 687.1 778.3 SOURCE: Ferguson and Kingsley 1972.

TIMBER PRODUCTS OUTPUT in MERRYMEETING BAY REGION 1971 Saw logs Pulpwood (000 rough cord) (000 bd-ft.) 1970 1971 MAINE 83,640 3,220.9 Sagadahoc County 1,867 18.5 15.1 Lincoln County 5,958 48.3 38.6 Cumberland County 13,597 49.4 44.0 Subtotal 21,422 97.7 SOURCES: Ferguson and Kigsley 1972. Bones and Dickson 1971.

FOREST STAND SIZE CLASSES (acres) Saplings- Non- Sawtimber Poletimber Seedlings Stocked Total Lincoln County 35,400 27,700 102,300 3,200 168,600 Sagadahoc County 38,900 291400 42,900 3,600 114,800 Cumberland County 13,500 10,200 23,400 100 47,200 TOTALS 871800 671300 168,600 6,900 330,600 %Total 26.5 20.3 50.9 2.0 100 SOURCE: SCS 1974

missing page 4-38

If proper care is taken in the mining and rehabilitation of sand and

gravel sites, the environmental and aesthetic impacts could be

minimized (see Chapter 8.0).

Manufacturing employs more workers in Maine than any other single

economic sector. This is true of the towns surrounding Merrymeeting

Bay as well. In 1970, 4,442 out of 13,558 jobs in the Bay towns were

in manufacturing industries (see Table 4-13 in Economic Overview).

The majority of these were located in Bath (1,333) and Brunswick

(1,394). Manufacturers located in these and other Bay area towns in

1974 are listed in Table 4-24.

The largest single employer in the Merrymeeting Bay region, the Bath

Iron Works, employs 3,700 people (March 1975 figures from Maine

Sunday Telegram 3/30/75). A spokesman for the company stated that

Bath Iron Works intends to maintain this level, increasing slightly

at least until mid-1976 (Maine Sunday Telegram 3/30/75). The number

presently employed is up 1;500 from the previous year and a half. At

that time (fall 1973) the company had completed a nearly two-year

effort to increase the shipyard's capacity to a more competitive

capacity. This included a doubling of the steel fabricating capacity

(East Brunswick), the installation of the 220-ton capacity crane in

Bath, and a number of production design alterations (Kennebec Journal

2/17/73). Despite Bath Iron Work's rising labor needs and the high

unemployment rate in the area (see Labor Force and Employment

section), the company has found it difficult to obtain enough skilled

workers to meet its needs. A recent attempt to recruit some 100

unemployed pipefitters met with little success. The reason, a

spokesman has conjectured, is that currently unemployed pipefitters

and plumbers are accustomed to a much higher wage scale in the

construction fields ($8.50 per hour) and are similarly accustomed to

winter lay-offs. They are thus unwilling to make a long term

commitment to a job that pays only half their normal pay rate ($4.50

per hour) when they expect activity in the construction fields to

pick up shortly (Maine Sunday Telegram 3/30/75).

1974 CENSUS OF MANUFACTURING Merrymeeting Bay No. TOWN FIRM EMPLOYED1 PRODUCT BATH Auerback Shoe Co. *501-600 women's snow boots Bath Canning Co. 51-75 canned sardines, froen shrimp Bath Iron Works *2500-37002 steel vessels Bath Printers, Inc. 1-4 printing Coastal Publishing Co. *11-25 newspaper Congress Sportswear Co. 76-100 mens, boys clothing Dispatchit 1-4 fuel delivery controls Dittmore-Freimuth 5-10 refurbishing electronic items Downeast Machine and Engineering 1-4 machine shop Down East Publications 1-4 newspaper MacDonald 3D Mag. Signs 5-10 plastic magneic signs Oakhurst Dairy Co. 26-50 dairy products, fruit drinks Redlon's Inc. 1-4 roof flanges, closet fittings Riverview Pattern Works O wood patterns, models BOWDOIN Clifford Card lumber BOWDOINHAM Corenco Corp. *26-50 mixed fertilizer Merrymeeting Farm 1-4 poultry processing Skowhegan Footwear, Inc 26-50 leather footwear BRUNSWICK Aeromarine Corp. 5-10 marine hardware Arrow-Hart, Inc. 26-50 molded plastic parts Auerback Shoe Co. *501-600 women's snow boots Bath Industries, Inc. *2501-3000 crushed machinery and parts Brunswick Publishing Co 51-75 newspaper, printing Engravers-Plastifab O engraving, die making J. H. French & Son 5-10 printing Health-Tex, Inc. 301-350 children's clothing Jay Corp. 201-250 artists/commercial brushes and equipment Keena Corp 5-10 reinforced gum tape Marriner Lumber Co. ---- lumber, ship timbers G. A. Peterson Co. *11-25 transit-mixed concrete, asphalt Pine Spring Water Co. 1-4 spring water, carbonated beverages Scandia Seafood Co. 26-50 processed shrimp Sewall and Son, Inc. 26-50 innersoles Tondreau's Bakery 5-10 bakery products Visi-Tray Mount Co. -- stamp mounts Washburn Lumber Co. -- lumber DRESDEN Rock-N-Stop O minerals, cut stones, jewelry Wood Products Co. O sweeping compound Jack Manchester O lobster trap stock RICHMOND Clarostat Mills 26-50 electronic components Charles A. Eaton Co. 301-350 men's dress and work shoes John Wallace (Brown's Mill) 1-4 lumber TOPSHAM Ronald Atwood 11-25 pre-cast cement products Granite Paving Co. 26-50 bituminous concrete, transit- mixed concrete Harpswell House 5-10 slate and wood desk accessories Hearst Corp (Pejepscot Div.) 401-450 newsprint, specialty paper Maine Times, Inc. 5-10 newspaper WOOLWICH Harvey's Machine Co. O machine shop Pine Tree Pattern O casting patterns 1. Zero indicates business is owner-operated. *Multi-unit Firm, figure covers all units. 2. Recent figures from Bath Iron Works in Maine Sunday Telegram, 3/30/75. SOURCES: Maine Department of Manpower Affairs 1973a, Maine Bureau of Forestry 1973.

The result is that the Bath Iron Works must train unskilled workers

to fill the vacant positions. This phenomenon is indicative of the

statewide shift from manufacturing to construction and other higher

paying fields (see Table 4-14).

Other major manufacturing firms which employ large numbers of Bay

area residents include the Auerback Shoe Company in Bath and

Brunswick, Health-Tex, Inc. (textiles) in Brunswick, Charles Eaton

Co. (shoes) in Richmond, and the Hearst Corp. Pejepscot Division, in

Topsham (see Table 4-24).

Table 4-24 indicates the economic importance of the manufacturing

sector in Maine, the Merrymeeting Bay region, and towns.

Significantly, Cumberland, Kennebec, and Androscoggin counties rank

among the top five tout of sixteen) in value of product manufactured;

while Sagadahoc and Lincoln counties rank tenth and sixteenth

respectively. Lewiston and Augusta to the north and west of the bay

rank second and seventh tout of 25) among towns in value of product

manufactured. Bath ranks tenth and Brunswick twenty-fifth, while all

other towns in the area produce less than the top 25 manufacturing

towns. What is of significance in these statistics is that they

demarcate quite vividly the inland corridor described by Barringer et

a1.(1972), an area of commercial activity directly related to the

interstate highway system. Lincoln and Sagadahoc counties to date

removed from easy access to this tranportation system have grown very

slowly in terms of commerce and industry as compared to Cumberland,

Androscoggin, and Kennebec counties linked by the Maine Turnpike (see

Table 4-26). Likewise, Lewiston and Augusta, directly adjacent to the

highway have grown into major commercial centers, while the

Merrymeeting Bay towns have languished in the backwaters. Bath and

Brunswick have managed to remain viable manufacturing centers due to

the activity of the Bath Iron Works. Completion of I-95 up the

western edge of the Bay will provide the access needed to spur

increased commercial and industrial activity (see also section 6.1,

Transportation). This implies that, with advanced planning, increased

commercial and industrial activity could be realized at little

environmental cost, and at great economic gain for the area.

MANUFACTURING--VALUE OF PRODUCT in MAINE and in MERRYMEETING BAY REGION 1967--1973 1967 rank(1) 1970 rank(1) 1973 rank(1) MAINE 2,155,818,875 2,449,793,135 3,208,407,588 Sagadahoc Co. 78,999,576 10 65,017,933 12 109,588,721 11 Lincoln Co. 18,379,744 16 19,406,646 16 20,15,406 16 Cumberland Co. 391,648,096 1 444,084,946 1 598,922,470 1 *Kennebec Co. 243,448,738 3 268,131,383 3 324,812,459 3 *Anduoscoggin Co. 228,055,603 4 232,228,581 4 284,774,034 4 MERRYMEETING BAY Bath 64,601,574 10 46,843,888 16 80,558,092 12 Bowdoin n.d. n.d. n.d. Bowdoinham 911,652 1,358,912 1,411,236 Brunswick 25,663,655 25 23,415,914 37,504,385 24 Dresden n.d. n.d. n.d. Richmond 3,640,349 5,328,764 12,251,972 Topsham 9,451,963 10,9T9,133 14,718,027 Woolwich n.d. n.d. n.d. *Augusta 70,114,554 7 79,476,066 7 95,742,151 8 *Lewiston 121,495,177 2 119,954,711 3 152,932,111 3 1. 16 Counties, Top 25 Towns. * not in study area. SOURCES: Maine Department of Labor and Industry 1967 Maine Department of Manpower Affairs 1973b.

INDUSTRIAL PLANT GROWTH 1967-1971 Merrymeeting Bay Region South Mid Central(1) Coastal(2) New Plants % 28.8 8.8 No. jobs 29.9 3.6 Plant Expansion % 28.3 7.9 No. jobs 18.0 4.8 Total Growth Plants 28.5 8.3 Jobs 24.1 4.2 1. Androscoggin and Kennebec counties primarily 2. Lincoln and Sagadahoc counties SOURCE: Maine Dept. of Economic Development in Barringer et. al, 1972,

One of the fastest growing economic sectors in Maine is contract

construction. Between 1960 to 1970 the number of jobs in this sector

grew by 23.6 percent, and between 1970 and 1973 it grew by an

additional 15.5 percent. This represents a 42.9 percent increase from

1960 to 1973 (see Tables 4-12 and 4-13).

In the Merrymeeting Bay area the number of persons holding contract

construction jobs increased from 530 in 1960 to 882 in 1970, a 66.4

percent increase (see Table 4-14). It is probable that many of these

jobs were held in companies outside the Bay towns as a recent

telephone survey of general contractors in the area revealed that in

these towns a maximum of 300 jobs were available through some 25

companies (many of which are owner-operated). The largest single firm

is Harry Crooker and Sons, Inc., in Brunswick which employs from 45

to 100 persons depending on the season. The second largest firm is

Reed & Reed in Woolwich which employs from 38 to 80 persons. All

other firms employ less than 10 persons throughout the years.

Section 6.4.2 of this report details the nature of the building

contractors in the area. There are no large scale operations. The

largest to date are builders that construct from 10 to 20 units per

year, and these are only three in number. Currently the depressed

economic conditions are slowing housing construction in the area.

Other construction businesses in the area are involved in road

building and maintenance, grading, backhoeing, etc.

As I-95 is completed and economic conditions improve, the

construction businesses in the area are expected to see substantial

activity. Because of the nature of the construction firms currently

in business in the area, the type of development most likely to occur

will be a proliferation of single family homes along major routes,

the result of little planning. Without planning and building controls

on the part of the towns, this incremental growth could lead to the

costly and inefficient use of land.

Service industries include medical and health. services,

educational services, hotels and rooming houses, auto repair

services, amusement and recreational, agricultural services, legal

services, other professional services, miscellaneous repair services,

non-profit membership organizations, etc. Between 1960 and 1970, the

jobs in the service sector statewide increased by 42.1 percent. In

Merrymeeting Bay between 1960 and 1970, this sector showed a 32.6

percent increase. Since 1970, the state has experienced an even more

rapid growth rate in service industries showing a net growth from

1960 to 1973 of 78.7 percent (see Tables 4-12, 4-13, and 4-14). How

this has been reflected in the Bay area is not known.

The Brunswick Naval Air Station has a significant impact on the

economic activity in the Merrymeeting Bay area and in the state as a

whole. In 1973, it was estimated that the Station generated 19.5

million dollars each year in military and civilian salaries, utility

service, materials expenditures, and special contracts (Kennebec

Journal 2/17/73). Besides employing some 2,900 military personnel at

a cost of $12.5 million per year, the Station also employs about 325

civil service personnel at an annual cost of $3.6 million.

In addition to the military and civilian payrolls, the Station spends

about $400,000 annually on contracts (road maintenance, housing,

etc.); $2.2 million for materials and some $800,000 for utilities and

other operating expenses. Most of these monies go to Maine firms.

An increase or reduction in the size of the Naval Air Station could

have significant results on the economy and on the environment.

Presently, it is suspected that a substantial housing demand is

created by Naval Air Station employees.

From 1968 to 1973, the number of jobs in Maine in the trade

industries increased by 37.3 percent. In the Merrymeeting Bay area,

from 1960 to 1970, a 20.4 percent increase was shown (from 1,773 to

2,136 jobs; see Tables 4-12, 4-.13, 4-14).

The number and type of wholesale and retail businesses in the area

are too numerous to detail. They include gas stations and automotive

parts stores, grocery stores, hardware stores, restaurants, drug

stores, antique shops, clothing shops, furniture and appliance

stores, department stores, and many specialty shops to name a few.

The town of Richmond contains 16 such establishments; Dresden, 12;

Bowdoinham and Bowdoin, a similarly small number; while Topsham,

Brunswick, Bath, and Woolwich together contain hundreds of such

businesses. Wholesale firms number far fewer than retail firms.

The economic importance of this sector is shown in Table 4-. In 1973

Sagadahoc County recorded about $21,000 in taxable sales; Lincoln

County, $38,000; and Cumberland County, $502,000.

Taxable Sales-Coastal Counties (in thousands of $s) CUMBERLAND LINCOLN SAGADAHOC 1964 $219,581 $16,426 $11,290 1965 258,831 18,269 12,354 1966 291,706 19,363 12,220 1967 307,300 19,608 11,698 1968 335,303 22,318 12,515 1969 372,662 24,628 13,908 1970 379,755 27,360 15,485 1971 394r691 31,343 16,577 1972 445,155 33,842 18,696 1973 502,129 37,834 20,911 SOURCE: Department of Taxation, unpublished data. The importance of tourism in retail and wholesale sales in the Merrymeeting Bay area has been indicated in a study called the "Economic Importance of Recreation Along the Maine Coast" (Veazie 1971). Table 4-28 presents the results of that study.

RETAIL SALES OF RECREATION-RELATED STORES 1958 and 1967 1958 1967 INCREASE (millions of dollars) (percent) STATE OF MAINE 266.5 352.5 32.2 Sagadahoc Co. 5.9 7.2 22.0 Lincoln Co. 6,0 7.8 30.0 Cumberland Co. 48,3 59.0 22.2 Kennebec Co. 11.1 15.4 38.7 SOURCE: Veazie 1971.

It is likely that the bulk of the activity within Sagadahoc, Lincoln,

and Cumberland counties occurs in the coastal areas, not within the

study area. However, as Kennebec County indicates, inland areas are

not without significance. The link provided by I-95 between the coast

and inland areas will undoubtedly result in increased

recreation-related traffic in the area, if not increased recreational

activity in the Bay area itself.

The portion of the recreational sales listed above which can be

attributed to summer tourism is not known. However, this could be

approximated from the following table which lists selected year-round

taxable sales and breaks out those generated during the summer

tourist season for Sagadahoc, Lincoln, Cumberland, and Kennebec

counties. Data are for the year 1969 showing percent increase since

1960.

TAXABLE SALES IN THE MERRYMEETING BAY REGION 1960-19691 ANNUAL % INCREASE SUMMER(2) % INCREASE ($000) 1960-1969 ($ 000) 1960-1969 STATE OF MAINE 1,185,140 65.0 562,059 64.7 Cumberland Co. 305,555 78.9 Sagadahoc Co. 14,073 31.5 152,4043 77.9 Kennebec Co. 68,147 85.0 Lincoln Co. 22,510 74.2 e = Partly estimated 1. Food, lodging, apparel, general merchandise, automobiles, furniture, building materials 2. May--September 3. Represents 37 percent of total annual sales of $410,285. SOURCE: Veazie 1973.

Thus, it would appear that in 1969 tourism had little impact on

taxable sales in the Merrymeeting Bay region. In planning for the

future of Merrymeeting Bay, consideration should be given, however,

to a probable increase in the demand for retail stores from increased

traffic, both tourism-related and residential. If proper planning

precedes the development of these establishments, their effect can be

made positive with real social and economic benefits to the

communities. If, on the other hand, the pressures to increase these

businesses are left unguided, haphazard, ill-planned growth could

result.

In planning for the future of the Bay, the following findings

regarding economic activity are significant:

1. Presently the manufacturing sector supplies a predominance of the

jobs in the area.

2. Economic activities which are increasing include public

administration/government, construction, service, and trade. In

looking to attract business, these hold the greatest promise of

continued activity and should be preferred over manufacturing which

has been declining in importance state-wide since 1960.

3. Resource-based industries traditionally have been significant in

the Bay. Today, agriculture and forestry are the two most significant

natural resource-based commercial activities. Agriculture faces grave

economic conditions which are reducing its profitability and

concerted state and local action may be needed to ensure that prime

agricultural lands are not lost to development.

4. Forestry operations in Merrymeeting Bay have been geared to short

term economic gain and not long term productivity. Incentives for

proper forest management are needed to protect the future forest

stock and to ensure that undue erosion and sedimentation are not the

result.

5. Increased development will bring increased utilization of local

sand and gravel resources. Proper controls to require rehabilitation

of abandoned sites could alleviate the negative impacts of these

operations.

6. Towns will become increasingly bedroom community-oriented unless

effort is made to attract new business and industry. With the new

linkage to the main commerce corridor, I-95, towns could stand to

reap substantial benefits, if guided according to sound land

management principles (such as in areas suitable for development with

proper access and buffered from residential areas).

7. Tourism has not been a prime activity in the Merrymeeting Bay

area. However, increased traffic from I-95 will generate demands for

retail trade and services which ought to be guided to avoid conflict

with other incompatible uses.

8. Residential development pressures will increase contract

construction, which, if left unguided, could result in haphazard,

ill-planned growth. The present size and character of contract

construction businesses in the area make it unlikely that this sector

will assume the planning functions required for development to result

in efficient well-conceived growth. The towns must assume this

responsibility and institute strong controls as to the location,

density, and type of development allowed, based on sound planning

principles.

This section will examine the tax structures of the towns around

Merrymeeting Bay to define how taxation affects land use decisions

and the social structures of those towns, In the past, property taxes

have borne the major burden of municipal expenses. This has put undue

pressure on landowners to sell or subdivide, or has caused, in the

least, financial hardship. The following discussion will describe the

history of taxation procedures around the Bay and how recent

legislation has affected these.

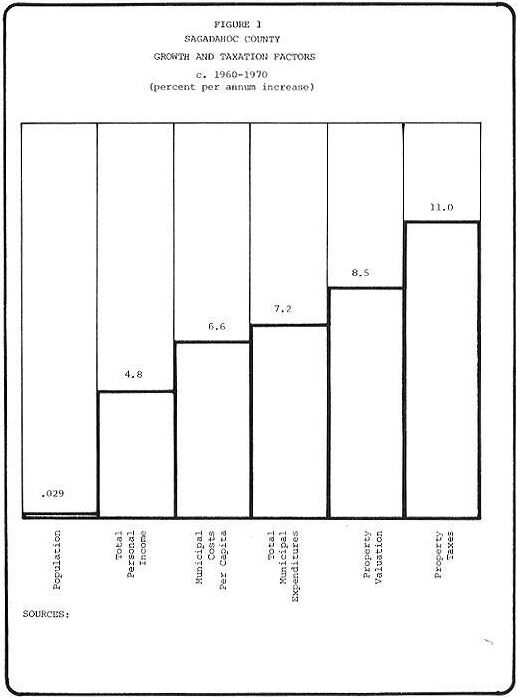

Municipal taxes in the Merrymeeting Bay region have been

increasing at a rate of 7 percent per year since the late 1950s.

Total municipal expenditures in Sagadahoc County have increased from

$2,304,000 in 1957 to $3,971,000 in 1967 (Veazie 1973). At the same

time the growth of incomes in the area has not kept pace with the tax

demands they must bear. Total personal income has increased at a rate

of 4.8 percent per year, from $52.5 million to 1959 to $82.6 million

in 1971 (see Figure 1, and Table 4-30).

This rise in municipal taxes results from the rapidly escalating

costs of principally two services: education (the cost of which rose

68 percent between 1957 and 1967) and highways (which required an

additional 52 percent in budget in that same period). Meeting the

high costs of education required an average of 50 percent of the

local budget in Sagadahoc County in 1967. By 1973 this had risen to

nearly 60 percent with some of the smaller towns contributing upwards

of 70 percent to education (see Table 4-31). Road construction and

maintenance, another major expense, while growing substantially has

been met increasingly with state aid. Education costs, on the other

hand, until recently, have been almost totally the burden of

municipal governments. Proportionately, roads required about the same

share of municipal expenses in 1973 as in 1967, although total costs

have increased. This may be subject to change, however. The recent

budget

Tuends in Municipal Revenues and Expenditures in Sagadahoc County 1957--1967 (OOO's dollars) % Change 1957 1967 1957-67 EXPENDITURES Total 2304 3971 72.3 Education 1138 1911 67.9 Highways 400 607 51.7 Police & Fire 233 307 31.7 REVENUES : Total 2391 4047 69.2 Local Sources 2015 3190 58.3 Property Tax 1614 2914 80.5 SOURCE: Veazie . 1973.

MUMICIPAL EXPENDITURES 1973 (000 dollars) Town County Education Roads Govt. % Govt. Protectionl % I Other % Total Bath 2,409 54 185 4 337 8 60 1 422 9 1,031 24 4,444 Bowdoin na na na na na na na na na na na na na Bowdoinham 201 62 49 15 24 7 5 2 13 4 29 10 321 Brunswick 3,547 54 448 7 199 3 52 1 658 10 1,644 ; 25 6,548 Dresden 182 66 46 17 13 5 5 2 1 negl 28 10 274 Richmond 609 69 74 8 42 5 7 1 58 7 87 10 877 Topsham 934 60 152 13 50 4 22 2 139 12 105 9 1,192 Woolwich 352 69 58 10 11 2 7 1 16 3 126 15 571 1. Police, fire, ambulance, street lights SOURCES: 1973 Town Reports submitted to the state Legislature did not include town road improvement funds or snow removal funds and towns may be called to bear an increasing share of road maintenance and construction costs.

Local governments have met the rising costs of municipal services

largely through the property tax. Between 1957 and 1967, the portion

of municipal costs borne by property taxes grew at a rate of 8

percent per year.

The picture is dramatized when one examines the actual property taxes

assessed since 1960 (Table 4-32). In Sagadahoc County, proper-ty

taxes assessed rose an average of 110.4 percent between 1960 and

1970. In the Bay area, this increase ranged from 40.3 percent in

Bowdoin to 179.4 percent in Dresden. The valuation of taxable

property for this period rose 93.3 percent in Sagadahoc County as a

whole, less than the increase in assessed taxation (see Table 4-33).

Only in the towns of Bowdoin, Bowdoinham, and Woolwich did the

increase in evaluation exceed the increase in taxation for this

period, as shown in Table 4-32. Elsewhere, taxes rose as much as five

times faster than assessed valuation.

Since 1970, there has been some relief in this respect. By 1973,

state and federal revenue sharing and increasing state and federal

grant programs had lowered the proportion of total revenues

attri-butable to property taxes to 56% for the Merrymeeting Bay area.

There is great disparity, however, within the Bay area as one can see

from Table 4-34. The portion of tax revenues raised by property taxes

in 1973 ranged from a low of 39 percent in Richmond to a high of 81

percent in Bowdoinham.

The recent passage of a significant tax reform law, Maine's new

educational funding law (L.D. 1994), effective 1974, is expected to

further relieve the property tax of a substantial portion of its

major burden, education, for many of the towns in the state,

including most of the

PROPERTY TAXES ASSESSED BY MUNICIPALITIES 1960--1974 (OOO's dollars) Change 8 Change 1960 1964 1968 1970 1972 1974 1960-1970 : 1970-1974 Bath 1,138 1,302 1,898 2,318 2,583 2,679 103,6 15.5 Bawdoin 57 55 56 80 100 85 40.3 6.2 Bowdoinham 80 97 152 172 218 21S 115.0 23.8 Brunswick 1,223 1,471 1,946 2,807 3,240 3,194 129.5 13.7 Dresden 34 40 64 95 102 126 179.4 32.6 Richmond 130 161 196 258 309 324 98.4 25.5 Topsham 235 341 520 642 847 940 173.1 46.4 Woolwich 110 119 156 213 295 327 93.6 53,5 Sagadahoc Cty. 1,991 2,373 3,369 4,191 4,983 na 110.4 na SOURCE: Veazie 1973i

STATE VALUATION 1960-19761 (000 dollar) %increase %increase 1960-1961 1968-1969 1971-1972 1973-1974 1975-1976 1960-1972 1971-1976 Bath 51,200 56,860 61,200 68,500 86,800 20.0 40.5 Bowdoin 1,080 2,340 2,860 3,440 4,920 164.8 72.0 Bowdoinham 2,700 4,760 6,700 7,900 10,700 148.1 59.7 Brunswick 49,000 74,000 91,000 101,500 117,100 85.7 28.6 Dresden 1,520 2,720 2,800 3,160 4,800 84.2 71.4 Richmond 4,500 6,920 8,300 10,680 14,300 84.4 72.3 Topsham 12,900 21,320 28,200 34,060 42,600 118.6 51.1 Woolwich 3,800 6,200 9,000 11,280 16,350 136.8 81.7 Sagadahoc Cty. 43,360 46,350 59,730 83,840 n.a. 93.3 n.a. 1. 100 percent valuation SOURCE: Maine Bureau cf Taxation, Maine State Valuation 1960, 1968, 1971, 1973, and unpublished data for 1975.

Merrymeeting Bay towns. In 1974, the impact of the law was only

partially felt, but in 1975, the towns will feel the full effect as

shown in Table 4-35. With the exception of Richmond, all towns will

see a substantial reduction in the local contribution to education,

and all towns will receive a sizeable increase in state aid.

The problems inherent in a tax structure which depends on property

taxes as a primary source of revenues should be alleviated by such

acts as L.D, 1994 and programs such as state and federal revenue

sharing. Yet it seems inevitable that costs of providing municipal

services such as roads, protection, water and sewerage will rise and

property taxes will continue to rise, although not as drastically as

in the past, to meet these.

The impact of rising property taxes is felt acutely by the elderly

who live on limited incomes and by families who have been typified as

"land rich and money poor." In the past, rising property taxes have

caused many of these families to sell off portions of their land or

in the least to bear substantial financial hardship. In 1971, the

state of Maine acted to relieve this problem by enacting the Elderly

Householders' Tax Relief Act. This act, effective in 1972, provides

for a direct grant to those elderly persons lover age 65 if male, 62

if female) maintaining homes, whether rented or owned, with a

household income of less than $4,000 annually. In 1972 the average

recipient was paid $104. This law should help alleviate the property

the tax burden for low income elderly citizens.

However, assistance of this Sort is not available to other types of

low income landowners, and this could well be a major problem in the

area. Rising property tax burdens could result in the break up of old

family estates, through the gradual selling of small parcels or

through sale of the entire property. Either could constitute a

regrettable loss to the Bay area.

Throughout the United States, the loss of farmland due to rising

pro-perty tax assessments has been identified as a serious problem.

An essential resource has been eroded by developmental pressures

which place the value of farmlands located in close proximity to

growth centers at a level equal to residential, commercial, or

industrial land. Taxes rise accordingly, farmers cannot meet the tax

costs, and the selling of small lots or outright sale of the entire

farm result.

Many states have taken steps to alleviate this problem by allowing

farmland to be taxed at its current use value rather than at its

potential value for development. In Maine a law such as this was

passed in 1971, called the Farm and Open Space Land Law. Effective in

1972, this law applies to "any tract or tracts of land including

woodland and wasteland constituting a farm unit of at least ten

contiguous acres on which farming activities produce a gross income

of at least $1,000 per year for three of the five calendar years

preceding the date of application for classifications." The state

issues guidelines to local assessors on the value of such lands. Once

lands are classified under the law, a change in use will result in a

penalty which would recapture past taxes for the period of

classification or ten years, whichever is less. In the Merrymeeting

Bay area, four farms have been classified under the law since it

became effective in 1972, including a 949-acre farm in Bowdoinham and

three farms in Brunswick totaling 352 acres. Two of the latter were

classified in 1974 whereas the others were classified in 1973.

Unfortunately, the economic problems of farmers, discussed in Section

4.4, are such that many farmers may be reluctant to give up the

option of selling off a portion of their land in order to avoid going

out of business, or in order to get out of an uneconomic situation

entirely. The fact that their land constitutes their only alternative

source of income, and that from year to year the economic conditions

nation-wide influence their ability to earn a living may be reducing

the effectiveness of the Farm and Open Space Land Law. It is also

true than many farmers do not know about the Farm and Open Space Law.

Ad-ministering a questionnaire to a sample of Maine farmers may point

out conclusions on why they have not utilized the law.

One of the problems which arise out of a property-based tax system

is that local citizens and officials are tempted to attract large

businesses and industries to their town in order to relieve the

general property tax burden. This could result in a situation where

non-monetary assets such as a clean environment or aesthetic features

are adversely affected.

While this has not been evidenced as a real problem to date in the

Merrymeeting Bay area, the potential might exist as I-95 is completed

and good transportation access becomes an attractive feature for

business. The state of Maine has recognized the problems inherent in

towns attracting businesses for tax benefits, and in 1973 enacted

what was called the Additional State Property Tax Law (Title 36, Sec.

455). This law, which became effective in 1974, attempts to phase the

local tax on business inventories out of local revenues and use it,

within a three-year period, to augment state revenues. The law allows

towns to continue receiving business inventory tax revenues from

businesses at that level which existed in 1973. That is, a town is

guaranteed, after three years, to receive state reimbursement for the

amount of revenue formerly obtained through the local business

inventory tax. Towns will not be able to tax new businesses for

inventory in the future, however. Despite this move to reduce the

temptation to accept businesses solely for tax reductions, towns may

still envision substantial tax benefits from business in terms of

increased valuation in land and buildings, and hence a lowering of

overall tax rate. Table 4-36 compares tax rates by town in 1972 and

1974. While towns may benefit from business developments in some

instances, care should be taken in evaluating the tax burdens imposed

by these developments as well as the social and environmental

consequences.

MUNICIPAL TAX RATES 1972-1974 Merrymeeting Bay Area Rate of Full Value* Rate of Full Value* Assessment Taxation Tax Rate Assessment Taxation Tax Rate Ratio (%) (Mills) (Mills) Ratio (%) (Mills) (Mills) Bath 80 45.00 37.70 60 42.00 25.57 Bowdoin 7 31.40 29.08 6 227.00 40.58 Bowdoinham 100 31.00 27.59 100 28.00 37.08 Brunswick 70 40.30 31.92 55 40.30 31.77 Dresden 45 64.00 32.28 50 53.00 25.10 Richmond 50 36.00 28.96 821 34.00 32.98 Topsham 71 37,00 24.87 50 38.50 36.23 Woolwich 3 102,00 26.17 20 103.00 34.50 *State Valuation (100%) divided by total tax revenue of municipality. 1. 1973 ratio SOURCES: Maine Bureau of Taxation, unpublished data for 1974. Maine Bureau of Taxation, 1972 data in .Veazie 1973. Reed & D'Andrea staff calculations for 1974 full value tax rate.

Just as farms may be subject to growth pressures and higher taxes,

forested lands may also. To alleviate this pressure on one of Maine's

most valuable resources, the state enacted the Tree Growth Tax Law in

1971. In its amended version, the law requires woodlots greater than

500 acres to be classified by assessors as forest land and allows

woodlots less than 500 acres and greater than 10 acres to be so

classed at the owner's request. Lands classed as forested are to be

taxed according to their value as woodlots rather than fair market

value, if the owner agrees to keep the land in its current

use--forest management. Failure to do so would result in a penalty

equal to the tax advantage gained while classed as forest land. In

the Merrymeeting Bay area, two parcels were classed as tree growth in

1974 (town of Brunswick), totaling 67 acres. These normally were

taxed (1972) at $786, but with the Tree Growth Tax Law, they are now

taxed at $40 (combined). The effectiveness of the law in keeping

forested land in production in Merrymeeting Bay is presently

ques-tionable as there is a noticeable lack of response to it. As

with the Farm and Open Space Law, many farmers do not know about the

Tree Growth Tax Law. The issuance of a questionnaire to a sample of

Maine farmers could more effectively conclude why more do not utilize

it. Apparently the profits gained by cutting and selling off lots for

development are greater than the potential tax savings. Another

factor affecting its effectiveness is the profitability of forest

management which fluctuates. In the future the law may well be a

determining factor in keeping forest lands in resource management if

taxes continue to rise.

Tax structures represent significant forces affecting land use

decisions and alternatives in an area, Recognition of this elementary

fact is essential if local and state governments desire to affect

proper land use. The following summarizes the major points of the

preceding discussion with reference to their planning implications:

1. Education has been a major burden for local taxes, particularly

property taxes, until the recent enactment of L.D.1994. This will

alleviate the education burden in all towns in the Merrymeeting Bay

area, While in some parts of Maine the effect of this law has been to

reduce the willingness or ability of towns to allocate monies for

conservation activi-ties such as public acquisition, increased

planning, and better enforcement procedures; this is not the case in

Merrymeeting Bay. Here the tax burden has been relieved and attitudes

are open for a reallocation of tax monies.

2. Another major tax burden has been the construction and maintenance

of roads. Until the present year (1975) the state has contributed

heavily towards town road improvement and snow removal. It is

difficult to assess whether the cutback will be temporary or long

standing. In either case, towns may wish to consider including a

requirement for developers to contribute to road service, as a means

of alleviating this burden.

3. Property tax pressures are most acutely felt by the poor and

elderly landowners, The state has provided some relief to elderly

householders with annual incomes less than $4,000. This is not enough

to avert the continued break up of large family parcels due to

economic duress. Some parts of the Bay will be best protected by the

continuation of large ownerships. This could help alleviate adverse

impacts in areas not suited to development or could simply help to

maintain the rural, undeveloped character of the Bay. Instituting a

mechanism whereby landowners could sell development rights to the

state or local governments would greatly alleviate this problem.

4. Similarly, farms are subject to development pressures. The Farm

and Open Space Land Law is not enough to avoid the continued break up

of farms. More drastic subsidies are needed and more liberal

financing.

5. Tax pressures are a reason for many towns to attract new business.

New business brings, generally, tax relief. In order to avoid a

situation where a town incurs expenses for a business incentive which

it cannot later recoup, a set of guidelines should be drawn up

detailing how all costs as well as benefits are to be surmised prior

to commitment to a business.

American Forestry Institute. 1972. Present forest land utilization

for the New England Region and projections for the future. AFI, New

England Natural Resources Center, Boston. Barringer, Richard, et al.

1972. A Maine manifest. Tower Publishing Co., Portland.

Bones, James T. and D. R, Dickson. 197. Pulpwood production in the

northeast--1970. U.S.D.A. Forest Service Resource Bulletin NE-24.

Northeast Forest Experimental Station, Upper Darby, Pa. 35 p.

Dearborn, Vance E. 1974. Population estimates for 194. IN Resource

Development Highlights, Vol. IX, No. 5, Cooperative Extension

Service, Univ. of Maine, Orono.

Dearborn, Vance E. and Ronald J. Daigle. 1972. Maine population

changes from 1960 to 1970. Cooperative Extension Service, Dept. of

Agriculture and Resource Econ., Univ. of Maine, Orono. 17 p.

Dresden Planning Board. 1971. Preliminary report of the planning

board. Dresden, Maine 30 p.

Ferguson, Roland H., and N. P. Kingsley. 1972. The timber resources

of Maine. U.S. Forest Service Resource Bulletin NE-26, Northeast

Forest Experimental Station, Upper Darby, Pa. 129 p.

Ferguson, Roland H. and F. R. Longwood. 1960. The timber resources of

Maine. Northeast Forest Experimental Station, U.S.D.A., Upper Darby,

Pa. 75 p.

Harris, Curtis C. Jr. 1974. Projections of demographic and economic

activity by county by decade to the year 2000. Computer printout.

Univ, of Maryland, Baltimore.

Kennebec Journal. February 17, 1973. Bath Iron Works enjoying record

backlog of orders.

Kennebec Journal, February 17, 1973. Brunswick base means

$19,500,000.

Lord, Willis. April 1975. Personal interview, Department of

Agriculture, Augusta.

Maine Bureau of Forestry. L973. Maine primary forest products

manufacturers as of December 31, 1973. Bureau of Forestry,

Augusta.

Maine Bureau of Taxation. 1960. Maine State Valuation 1960. Bureau of

Taxation, Augusta.

Maine Bureau of Taxation. 1960. Maine State Valuation 1960. Bureau of

Taxation, Augusta.

Maine Bureau of Taxation. 1968. Maine State Valuation 1968. Bureau of

Taxation, Augusta.

Maine Bureau of Taxation. 1971. Maine State Valuation 1971. Maine

Bureau of Taxation, Augusta. 197 p.

Maine Bureau of Taxation. 1973. Maine State Valuation 1973-basis on

which state and county taxes are assessed during 1973 and 1974.

Maine Bureau of Taxation, Augusta. 206 p.

Maine Bureau of Taxation. 1975. Unpublished data on farm and open

space and tree growth tax lands. Bureau of Taxation, Augusta.

Maine Department of Agriculture. 1975. Unpublished data on farming in

Lincoln, Sagadahoc, and Cumberland counties for 1969 and estimates

for 1974. Dept. of Agriculture, Augusta.

Maine Department of Commerce and Industry. 1973. Maine economic data

book. Maine Dept. of Commerce and Industry, Augusta,

Maine Department of Commerce and Industry. 1973. Community investment

buildings, an approach to Maine's industrial development. Maine Dept.

of Commerce and Industry, Augusta. 45 p.

Maine Department of Commerce and Industry. 1974. Facts about

industrial Maine. Dept. of Commerce and Industry, Augusta. Maine

Department of Education and Cultural Services. 1975. Unpublished

files on local share to education. Department of Education &

Cultural Services, Augusta.

Maine Department of Labor and Industry. 1967. Census of Maine

manufactures. Dept. of Labor & Industry Bulletin 428. Augusta. 22

p.

Maine Department of Labor and Industry. 1970. Census of Maine

Manufactures. Dept. of Labor & Industry Bulletin 480. Augusta. 22

p.

Maine Department of Manpower Affairs. 1973a. 1974 Maine buyers'

guide.

Maine Dept. of Commerce & Industry, Augusta. 180 p.

Maine Department of Manpower Affairs. 1973b. Census of Maine

Manufactures. Dept. of Labor and Industry Bulletin 519. Augusta. 22

p.

Maine Department of Manpower affairs. 1975. Unpublished files on

employment and labor force. Dept. Manpower Affairs, Augusta.

Maine Guarantee Authority. n.d. Requirements for obtaining community

industrial building loans from Maine Guarantee Authority (MGA).

Augusta. mimeo.

Maine State Planning Office. 1973. Maine population projections.

State Planning Office, Augusta. 32 p.

Maine Sunday Telegram. March 30, 1975. Unemployed reject jobs, says

BIW.

N.A. 1973 Town reports for Bath, Bowdoin, Bowdoinham, Brunswick,